Is Mario Draghi a traitor?

Mario Draghi the lamb werewolf

Mario Draghi at the same time is not a man of finance, but he is a man of banks.

From 1985 to 1990 he was executive director of the World Bank.

In 1991 he was appointed Director General of the Treasury.

In 1992 he is one of the Italians invited on board the Britannia where he sells off Italy and is well rewarded as from 2002 to 2005 he was appointed Vice President for Europe of Goldman Sachs, to be then at the end of 2005 appointed Governor of the Bank of ' Italy.

It was 2011 when, with his famous letter, co-signed with Trichet, he helped to bring down the Berlusconi government and was subsequently appointed president of the ECB.

Many have raised the flag when Draghi was placed at the top of the ECB, with inadequate patriotism, completely disconnected from reality.

Mario Draghi is a banker, he does not wear the blue jersey and he is not the captain of the national team. He is a technician who thinks, lives and breathes as such.

His task was not to save the Italian public accounts or to pay some debt to Italy as some pathetic big babies have hoped. Rather, his intent was to extend the stock with the purchases of government bonds, not in the national interest, but in the survival of the Euro.

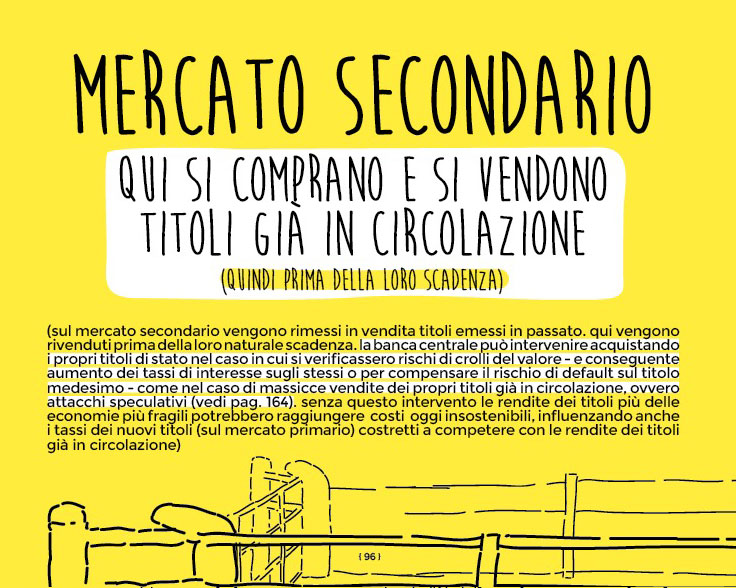

With the QE Draghi caused the European Central Bank (ECB) to buy public securities on the secondary market; a process explained in detail but simply in our easy explained economics book.

Below is a small taste of part of the explanation.

How the secondary securities market works

Effects of the ECB intervention

With the direct intervention of the ECB, a completely artificial demand for securities (including Italian ones) was created, which replaced the buyers who did not want to buy them.

In other words, thanks to Draghi's maneuver – absolutely notwithstanding the constraints of the ECB to which Germany and its peripheral countries were opposed – he was in fact able to make the ECB buy all those public bonds that no one wanted except at a high price from the public coffers. .

In this way, it affected the market for all public securities, not only the old ones (which circulate in the secondary market), but “by contagion” also the yields of future bonds.

What does all this talk mean in layman's terms? It means that the market for government bonds has been calmed or that the rates of those bonds have fallen and consequently also the annuities that the States will have to repay to the lenders, or to the market operators when these bonds will expire.

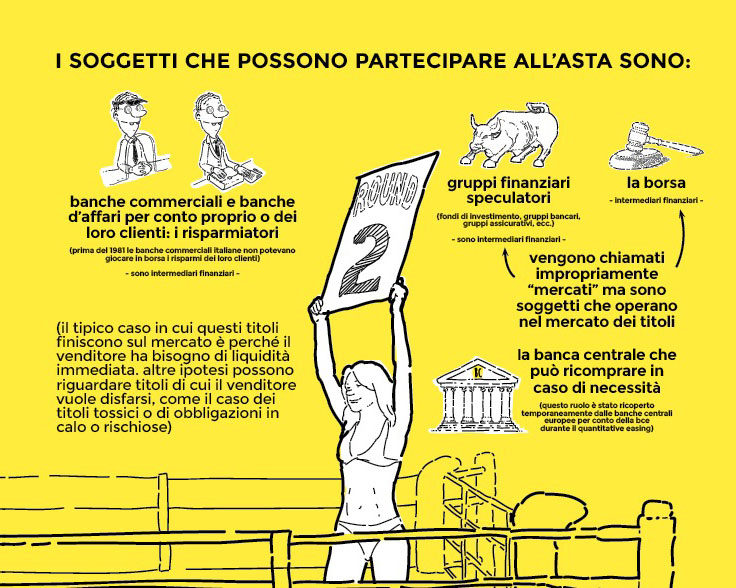

The role played by the ECB during QE is called the lender of last resort that we have described in this article and also in our book.

With the QE Draghi made sure that the public accounts of Southern Europe did not explode and thus averted the collapse of the eurozone and the return to national currencies.

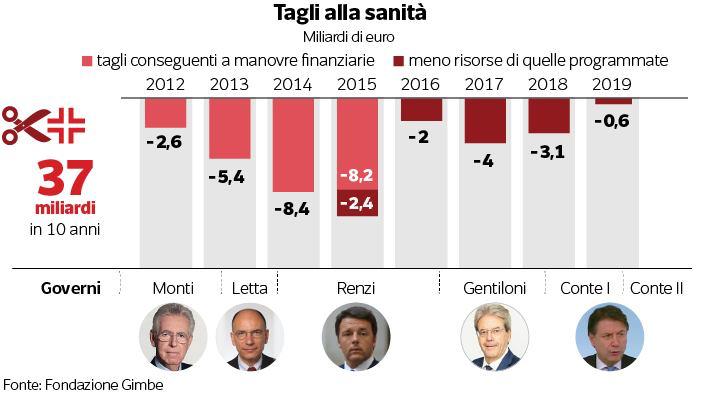

Mario Draghi and the cuts

So did Draghi serve Italy's interests? No, it served the interests of the creditors of the states which, if they defaulted, would have caused them huge losses and in fact the collapse of the markets themselves. That these interests coincided with the survival of public accounts is obvious, because large portions of the interests of the stock markets are based on these.

At this point I happened to be teased: Draghi is the savior of the country because by doing QE he avoided the (false) cuts linked to austerity.

Luca Menini does not know a significant enough fact.

Quantitative easing (QE) is monetary policy, not fiscal policy. It is the budgetary policies that lead to cuts and spending.

What determines how much and how to spend is determined by the state budget – that is, politics – and not the monetary issue by the Central Bank, whatever it may be.

“ Fiscal policy is not the responsibility of central banks and their governors. And in fact Draghi has never failed to urge the states with spending capacity to spend on investments, and not from today. "

In fact, does anyone appear to have stopped cutting public spending?

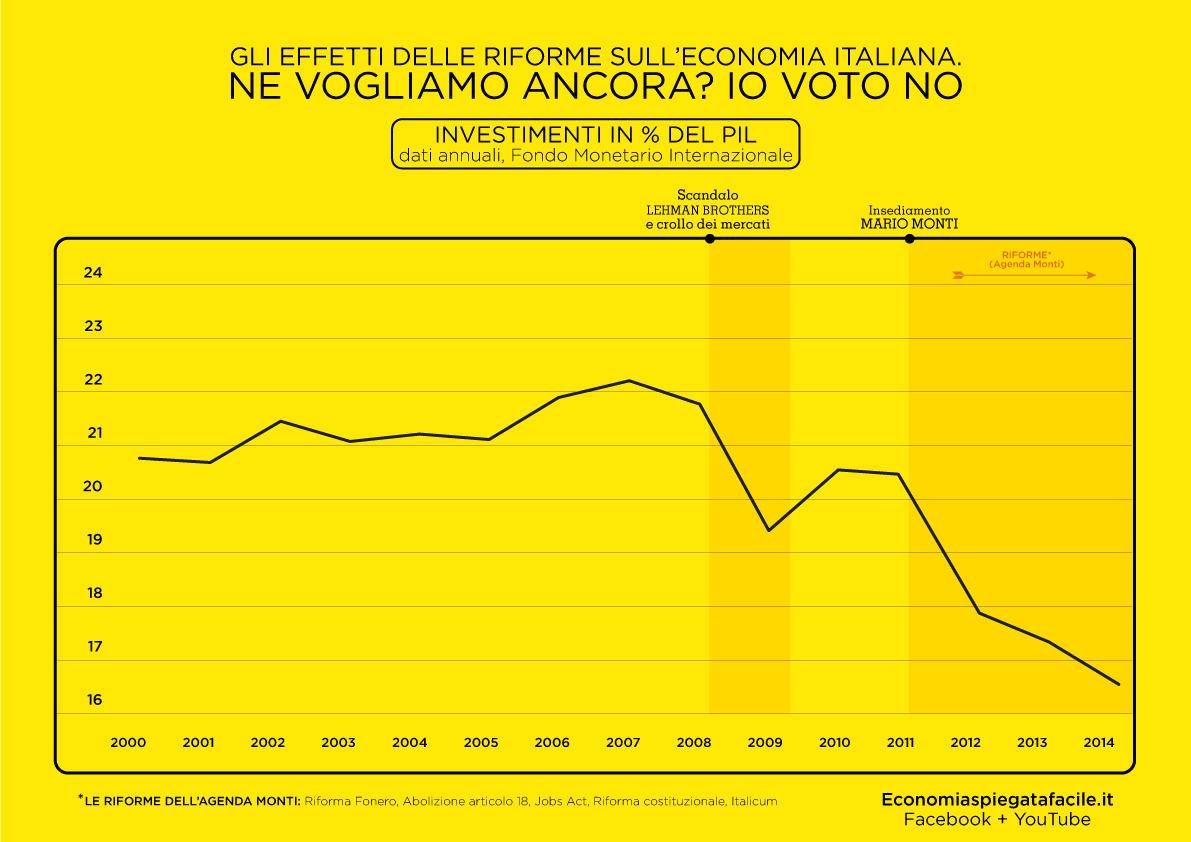

Investment chart 2000 – 2014

So how do Draghi's choices on monetary policies reconcile with the trend of these graphs?

Simple because the balance of public finances serves to guarantee creditors, not the well-being of citizens: while spending cuts are reduced, debt containment is guaranteed, which reassures the markets.

Result on the reduction of public debt? There he is:

Because, as the basic laws of the economy teach, if you cut public spending, you impoverish the country and a poorer country will have to contain expenses, consequently remaining behind the economies in which the most is invested. In the long run, the poor remain behind on all counts and will have to resort to new debt to try to keep up with the progress of competition.

In short, more austerity = more debt.

UNDERSTANDING THE ECONOMY IS FUNDAMENTAL

TODAY IT HAS ALSO BECOME EASY:

SECURE PAYMENTS

![]()

Did Draghi help the Italian economy?

If anyone has ever asked this simple question, perhaps they have not found certain answers.

We list some of them.

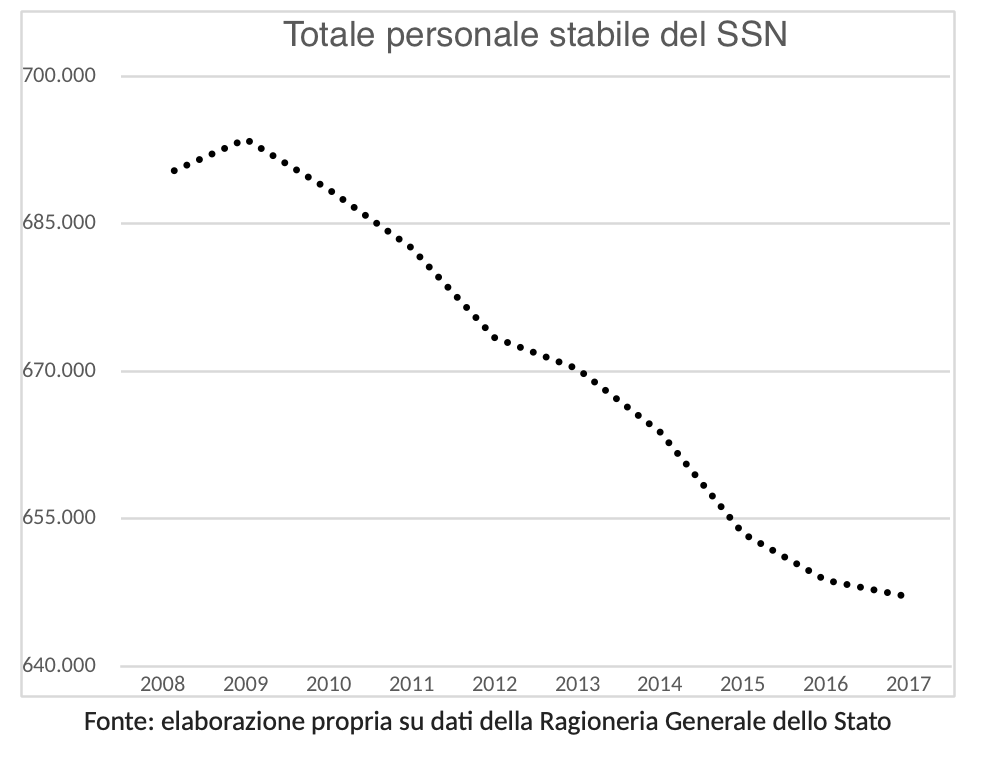

Too bad that spending cuts arithmetically equate to increases in health services, just to give an example.

Here is what we mean when we say that QE does not always correspond to adequate investments to face the changing times, such as, for example, the aging of the population or the modernization of infrastructures and transport (see the differences with Japan):

View? Despite the expansionary monetary policies of the ECB, restrictive investment policies continued to be implemented: to cut everything and raise taxes.

The cuts in healthcare have been accompanied by a reduction in hospital beds and a reduction in infrastructure. For the school it was reflected in the cuts on teaching materials for the school. For industry it manifested itself in the privatization of infrastructure, etc.

All stuff that you then have to pay for out of your own pocket. Not exactly a speech as a savior of the Fatherland.

So – in the current system – what remains in your pocket, thanks to a hypothetical tax cut (which never actually happened), you should spend in private structures!

And the story isn't over yet!

Raised by the Jesuits, a constant among several leading names in Italian politics today, he becomes a man of Goldman Sachs . And so far nothing secret or forgotten.

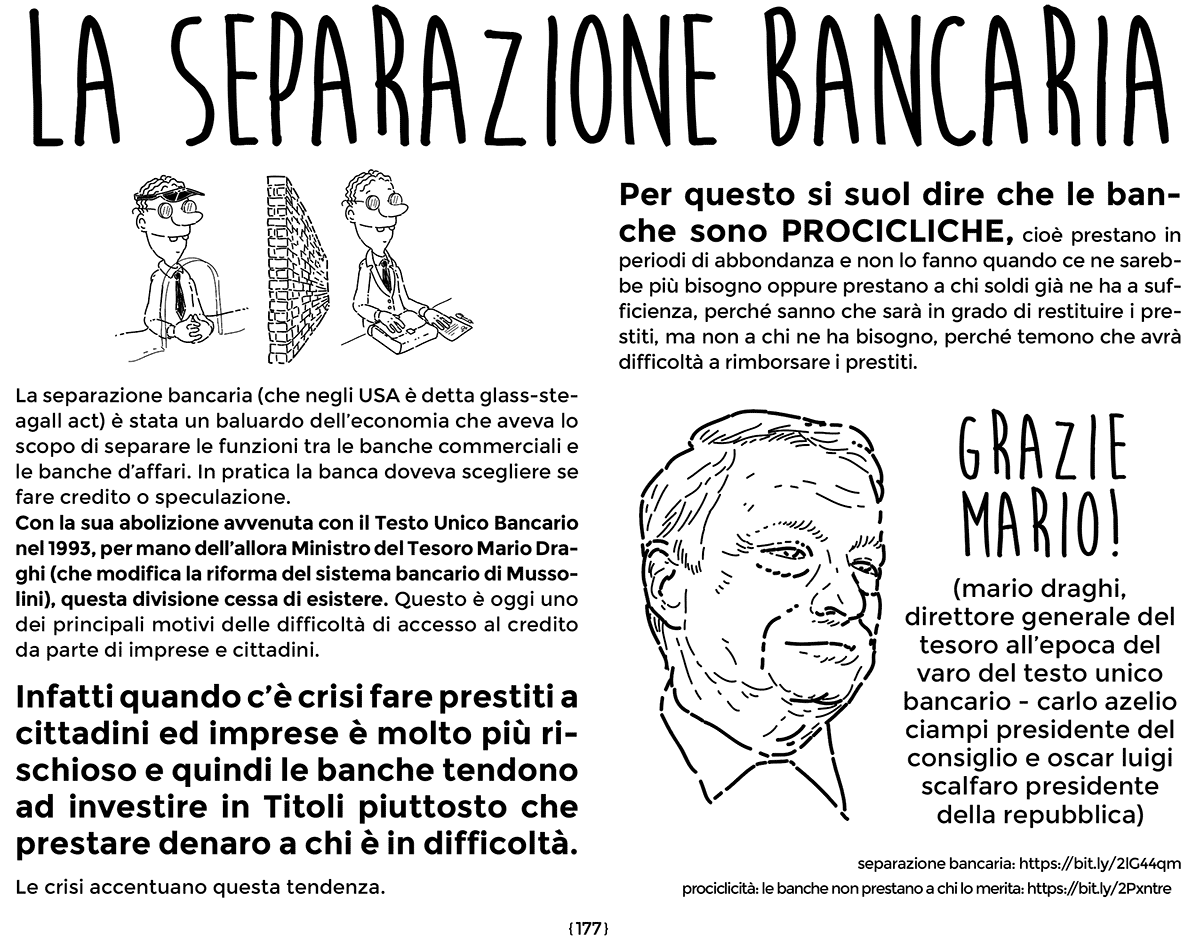

1993 banking separation

With its abolition with the Consolidated Banking Act in 1993, by the hand of the then Director General of the Treasury, Mario Draghi, this division ceases to exist. This is today one of the main reasons for the difficulty of access to credit by businesses and citizens.

Before the abolition of the banking separation, which took place in 1993 when the Prime Minister was Carlo Azeglio Ciampi, investment banks and commercial banks were divided by category and mission (either to provide credit in the real economy or invest in capital) and could not operate in a sector other than their own.

The effects of the cancellation of the separation is the main cause of the credit crisis.

It is not convenient for banks to lend money to businesses, businesses and families. Better to invest and also make savers invest in the stock exchanges. Less risk and more profits.

90's the wrong derivatives

When Mario Draghi was at the treasury ministry, on his proposal and implementation, Italy took out numerous derivatives on its debt. The data available to us indicate that up to 2015 Italy was exposed in derivatives on government securities for 163 billion.

On those 163 billion in derivatives purchased by the state, the losses were 37 billion!

The privatizations of the 1990s

Without going into the merits, which we reserve for this article , one of the aspects that distinguish Mario Draghi's vision from that of many others is that privatizations should serve to reduce the debt and not to reduce the deficit.

It seems a contradiction in terms but it is not.

In fact, if the deficit can be made at advantageous conditions, it does not mean that at the same time the debt cannot be reduced, if it produces disadvantages deriving from worse “contractual” conditions.

Too bad that the privatizations of Draghi, Ciampi, D'Alema and Prodi all worked out, starting with the gifts to friends of their political and business currents, see the IRI case one for all, except the reduction of public debt, as we can all well ascertain

In fact, that privatization campaign was a general sell-off of a large chunk of public capital.

1999, privatization of the sale of Autostrade to the Benetton family

(see in the sources at the end of the article)

2007, The hole of MPS for Antonveneta

In 2007 Draghi authorized the acquisition of Antonveneta by MPS.

Already at the time, the merger took place on the basis of overestimated figures.

The results achieved to date are these:

Between 2011 and 2017, the bank, which capitalizes less than 1.4 billion on the stock market, requested 18.5 billion from the market in the form of capital increases, of which 5.4 billion provided by the state.

With the loss of 1.69 billion in 2020, the losses accumulated by Mps in the last decade, starting from 2011, amounted to approximately 23.5 billion euros.

GIVEN THAT UNDERSTANDING THE ECONOMY IS CONVENIENT TO YOU?

CHOOSE THE SIMPLE, IMMEDIATE AND ECONOMIC WAY

SECURE PAYMENTS

![]()

2011, The letter of threats to Italy

It is August 5 when the storm that sweeps the stock exchanges pushes the increase in the stread between BTPs and Italians and German BUNDs, up to 389 points.

The then duo, outgoing president and president in pectore of the ECB Jean Claude Trichet and Mario Draghi wrote a private letter (which should have remained secret) to Silvio Berlusconi.

In this they express their concerns about the stability of the Italian system (whose collapse would involve the rest of the eurozone) "suggesting" solutions in no uncertain terms.

It is a real list of instructions listed point by point :

"In the current situation, we consider the following measures essential: …"

These include recipes for optimizing the public machine, education and justice, but also linear cuts in public spending and new privatizations, as well as a revision of the political-bureaucratic system that targets the abolition of the provinces.

But explicit reference is also made to the labor reform, that is to the pre-hecarization of workers to be implemented to help companies to be more competitive on a global level (even against those who exploit work or compete unfairly, see China):

"There is also the need to further reform the collective wage bargaining system, allowing agreements at the company level in order to tailor wages and working conditions to the specific needs of companies …"

The threat asserted that failing that, the ECB would not have continued the purchase of Italian BTPs on the secondary market (the first phase of quantitative easing), thus fearing Italy's default.

The day after that letter, Berlusconi and Tremonti will present themselves at the press conference – with closed stock exchanges – to announce the introduction of an extraordinary maneuver.

Andrea D'Ambra (president of the Active Generation association) wrote to the ECB asking to be able to read that letter and was answered on 7 September 2011:

"We're sorry, the letter must remain secret"

Thus it was that, with Draghi, a supranational body such as the ECB, not elected and above all without political aims, intervened in the political affairs of Italy. It goes without saying that Berlusconi – like it or not, democratically elected – was in fact removed to make room for Mario Monti .

Read the letter in full version

Failure to achieve the 2% inflation target

During his tenure, Mario Draghi was the architect of the famous quantitative easing we mentioned at the beginning. This operation led the ECB to buy government bonds (on the secondary market) and lower spreads. In practice it was the monetization of European debts.

However, his goal was also another, namely to achieve an inflation rate of 2% in the euro area.

Germany was opposed to this objective, which, being a creditor country, would have lost 2% of its credits.

Another nice favor to the very rich.

Today, while we are still in the midst of the Chinese virus pandemic, inflation has been pressing for some months for exogenous causes. It means that it is not a regulated phenomenon on a financial or monetary level, but that it is a phenomenon caused by external and uncontrollable agents. The ECB has no mandate to reduce unemployment or help the economy, businesses and households and it shows.

It has injected liquidity into the financial markets like never before and has not produced investments that have kept Italy in step with the needs that reality requires. The pandemic was the most striking manifestation of this.

It is another example of how the fact of not having worked to redistribute resources, but to guarantee the financial markets, has caused damage that today we all pay together.

The management of the pandemic in Italy by Mario Draghi

Called, exactly as it happened with Mario Monti, to fill the role of President of the Council of Ministers, without having first passed through elections, Mario Draghi will have to take care of ensuring the correct spending of EU funds ( PNRR ) by removing this task from the hands of politicians incapable that we have.

The whole story of how he handled the pandemic will be judged by citizens and history. However, some data give us the figure of how he approached this challenge.

Always with the usual empathy towards humanity and the choice of technical and political collaborators whose fruits are under the eyes of the statistics.

GET A SECRET ARCHIVE TO FISH FROM

MANY BEANS LIKE THESE:

ECONOMI / GRAM contains hundreds of this information. It is a paperback that helps you to remember all the most controversial news and how it turned out every matter concerning: economy, politics, covid, green economy, foreign. To never let yourself be put under – to gossip – by those who want to teach you how to be in the world.

SECURE PAYMENTS

![]()

Draghi was chosen to guarantee credibility with respect to the commitments that Italy will make on the Recovery fund. To ensure investors. Not for the common good.

Any public or private office he should hold will remain devoted to this mission. After all , Federico Caffè, his university professor of economics, a fervent Keynesian, told Nino Galloni: “Mario betrayed us”.

Or as Francesco Cossiga said: "He is a cowardly businessman":

This , precisely, means his “Whatever it takes”.

Full version of the article on economiaspiegatafacile.it

The series of, The traitors of Italy

![]()

Thanks to our Telegram channel you can stay updated on the publication of new articles of Economic Scenarios.

Is the article Mario Draghi a traitor? comes from ScenariEconomici.it .

This is a machine translation of a post published on Scenari Economici at the URL https://scenarieconomici.it/mario-draghi-e-un-traditore/ on Mon, 24 Jan 2022 08:52:40 +0000.