How industrial production will go in Italy. Confindustria report

What emerges from the report of the Confindustria study center on industrial production

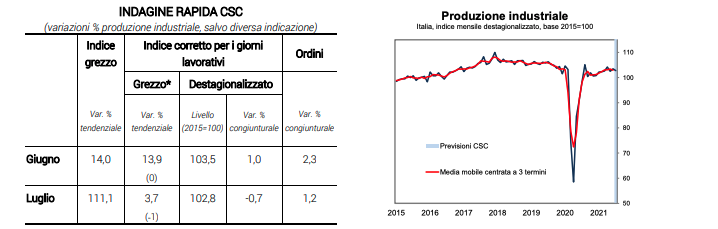

Italian industrial production grew in the second quarter at a rate close to that recorded in the first (1.0% vs 1.3%); the third part with a negative start: in July it is estimated a decrease in activity of 0.7% (after + 1.0% recorded by Istat in June) explained both by a greater use of inventories, necessary to satisfy the influx of orders, and from some bottlenecks in the supply along the international production chain due to the scarcity of some components and raw materials. Domestic demand shows greater vivacity than foreign demand. According to the qualitative surveys conducted in the first half of July, entrepreneurs continue to be optimistic, although fears related to new restrictions following the spread of the Delta variant are starting to affect medium-term expectations. The August confidence surveys could fully capture these concerns.

The CSC notes a decline in industrial production of 0.7% in July over June, when Istat recorded an increase of 1.0% over May1. The activity levels are slightly lower than those of February 2020. The cyclical variation in the second quarter is + 1.0%, after + 1.3% in the first, and the variation acquired in the third is -0, 5%. Production, net of the different number of working days, increased in July by 3.7% compared to the same month of 2020 (+ 13.9% in June). Orders in volume advance in July by 1.2% on the previous month (+ 8.8% on July 2020) and in June by 2.3% on May (+ 13.6% per annum).

The economic indicators relating to the third quarter continue to indicate a positive trend in industrial activity, with orders on the rise (especially in the domestic component) and favorable production expectations. However, it is not excluded that in the summer months there will be a slowdown compared to the dynamics recorded in the spring. According to the findings of the PMI Manufacturing survey (IHS-Markit), the effects of the scarcity of raw materials and components are beginning to emerge in Italy too, factors that have led to a blockage of global supply chains, causing bottlenecks in supply. in particular in some sectors (automotive, electronics, machinery). The worsening of the indicators relating to backlog and average delivery times of suppliers reflects these growing supply problems which tend to slow down the expansion of the business – despite an increase in orders – and create pressure on production capacity. Furthermore, second-round effects on Italian industry are probable deriving from the repercussions of these factors on the activity of our partners, first of all on Germany where production in July fell by 1.3% cyclically (against expectations of an increase of 0 , 5%), down for the third consecutive month. In the medium term, the risks arising from the increase in infections due to the Delta variant and from the prospects for the reintroduction of further limitations accumulate. In July, however, the survey on the confidence of manufacturing entrepreneurs – conducted in the first two weeks of the month – did not address these concerns and the index rose to historically high levels .

It is not excluded that in August there will be a first repercussion on the confidence of businesses and households. Already in the IHS-Markit survey, which was conducted in the second half of July, a sharp slowdown in expectations was observed, which fell to the lowest level since April 2020 due to growing fears of a resurgence of the virus and a tightening of restrictions. . The return of uncertainty risks becoming the main obstacle to the ongoing recovery.

This is a machine translation from Italian language of a post published on Start Magazine at the URL https://www.startmag.it/economia/come-andra-la-produzione-industriale-in-italia-report-confindustria-2/ on Sat, 07 Aug 2021 08:41:02 +0000.