China: rates unchanged, with a difficult path between deflation and liquidity trap

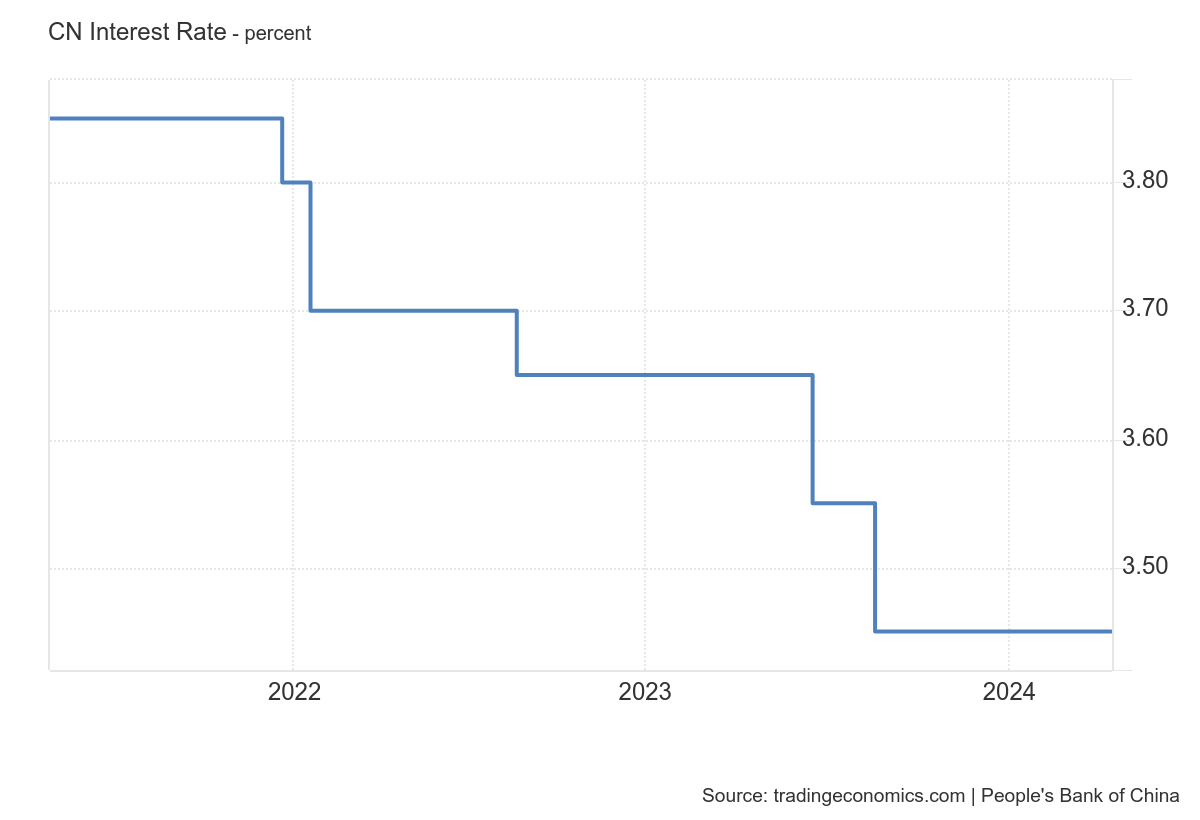

Today the PBOC decided to keep the LPR rates and the Loan Prime Rate, the reference for the credit sector, unchanged. This one-year rate, the reference for a large part of the banking system, has remained unchanged, and this is in line with market forecasts. Here is the relevant graph:

The five-year rate, which is usually the reference for mortgages, also remained unchanged at 3.95%. The PBOC has decided not to overdo the monetary stimulus, perhaps because it is realizing that, at this time, it is not as useful as a fiscal stimulus.

A big deflation problem

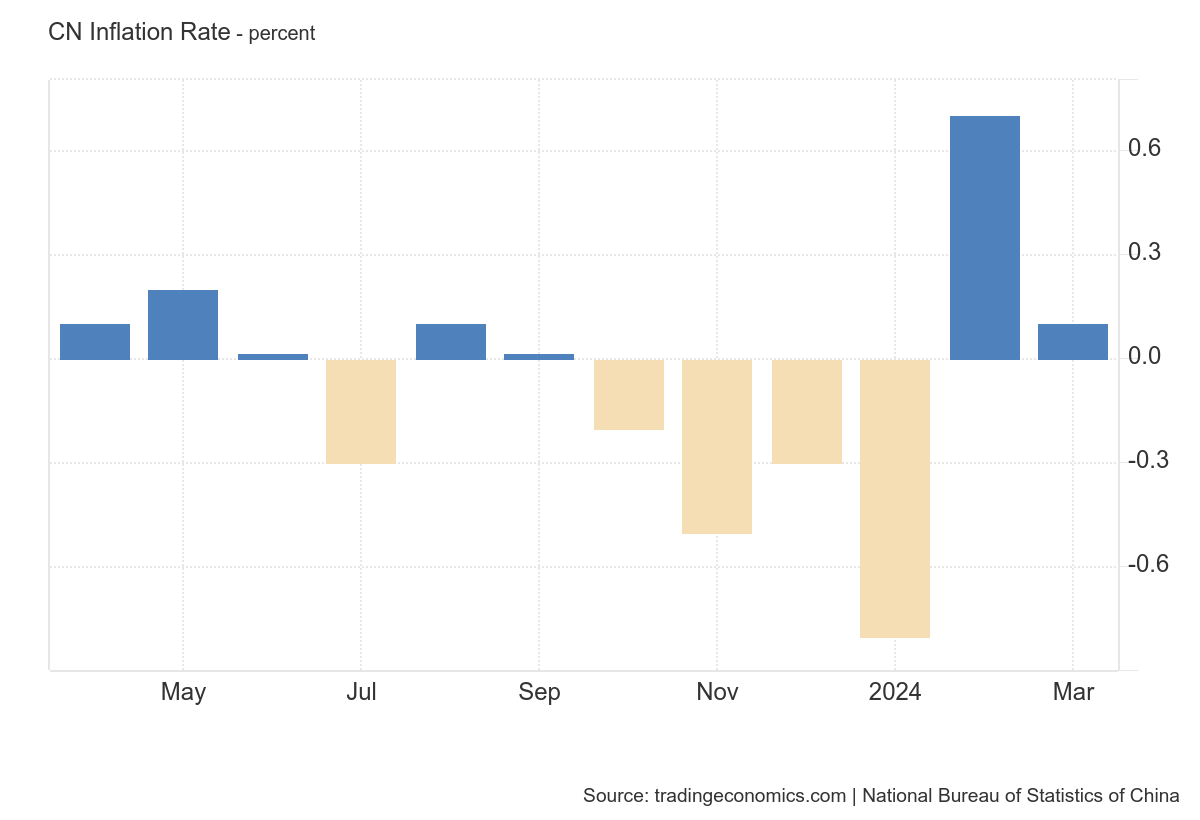

Now if 3.45% doesn't seem like a lot for China it is, in reality, a lot, because consumer price inflation is currently very low: in March it was 0.1%

In the last six months the highest annual inflation rate was 0.8%, so the rates set by the central bank are not only positive, but strongly positive.

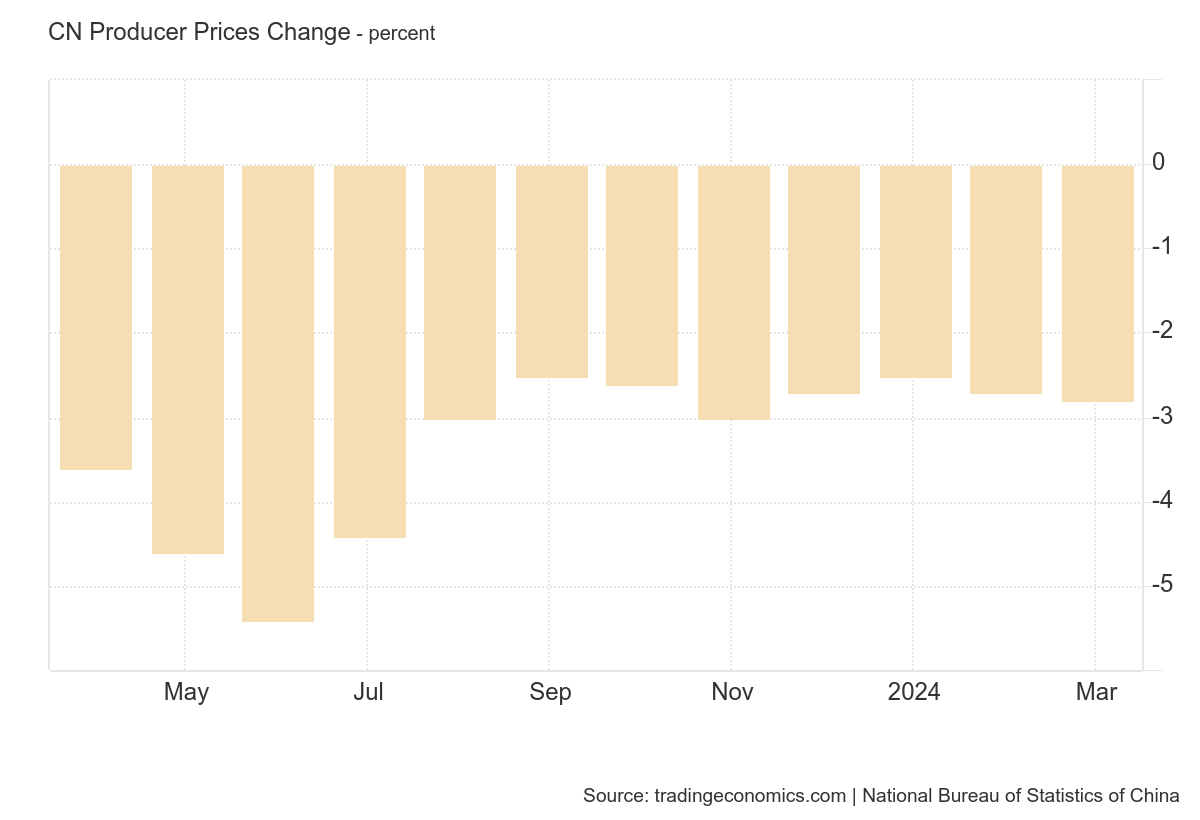

The situation of production costs is even worse, indicating that, in any case, there is a demand problem and a significant one. The reduction in producer prices cannot only be explained by greater efficiency, but also by a cut in margins, and this will ultimately lead to closures and layoffs

A lack of confidence fuels the liquidity trap

The problem is that the banking system is burdened with insolvencies and securities with zero or almost zero valuation. Not to mention the various Evergrande and Country Garden cases, the value of mortgage defaults grew by 43% and the number of assets seized by banks, including commercial properties, reached 793 thousand. But a healthy bank is not a real estate developer and these numbers are worrying. Even if the PBOC and the government guarantee the solidity of the credit system, resources are still cut.

In this situation, the danger of a liquidity trap, i.e. a situation in which the resources injected into the banking system by the Central Bank and lent to consumers do not turn into consumption, but are hoarded and remain unproductive, is very high. The Chinese are no longer buying apartments, which in any case have a productive activity behind them, but gold, which is only a safe haven asset which does not stimulate the economy, and this also explains the recent growth in the price of the precious metal.

However, gold is a disaster for the national economy, because it is the hoarding asset par excellence and the most productive. A nation could possess thousands of tons of gold, even at a popular level, and see hunger on the streets, because gold marginally develops economic activity.

What could the PBOC and the government do

The solution to the problem is not at all simple. There are recipes, but they are far from certain in their results.

- Buying Government Bonds: The PBOC may increase its buying of government bonds to increase liquidity and lower real interest rates. However, this would require coordination with the Ministry of Finance to increase the sale of debt and then this debt should be well utilized. Otherwise the liquidity would end up in the purchase of gold, i.e. in an unproductive and hoarded investment

- Expansionary fiscal policies: The Chinese government may implement bolder fiscal stimulus measures to increase aggregate demand, but this could increase the deficit-to-GDP ratio. That is, the money obtained from the sale of securities should be used for something useful and productive, not in useless infrastructures, empty shopping centers, ghost towns.

- Banking sector reforms: The PBOC could encourage banks to focus on their core business of providing credit and strengthen their balance sheets by improving financial supervision and risk management. This won't be easy.

- Measures to increase confidence: Improving transparency and communication by monetary and financial authorities could increase confidence in the system and encourage investment.

The challenges and unknowns:

The problem is that all of this is easier said than done. Directing investments exactly as the PBOC would like requires a detection and feedback system to understand where the money actually ends up.

It would also require the state to actually invest based on economic and non-political guidelines, correcting its priorities. It would then be necessary to increase public trust in the banking system to ensure that money flows back into productive investments. All not exactly simple steps. However, China must be able to overcome this impasse, even at the cost of putting aside some political priorities.

![]()

Thanks to our Telegram channel you can stay updated on the publication of new Economic Scenarios articles.

The article China: rates unchanged, with a difficult path between deflation and liquidity trap comes from Economic Scenarios .

This is a machine translation of a post published on Scenari Economici at the URL https://scenarieconomici.it/cina-tassi-invariati-con-un-diifficile-cammino-fra-deflazione-e-trappola-della-liquidita/ on Mon, 22 Apr 2024 11:14:25 +0000.