Because the comparison between Evergrande and Lehman is risky. Moneyfarm report

Who risks and how the Evergrande case will be resolved. The analysis by Roberto Rossignoli, Moneyfarm portfolio manager.

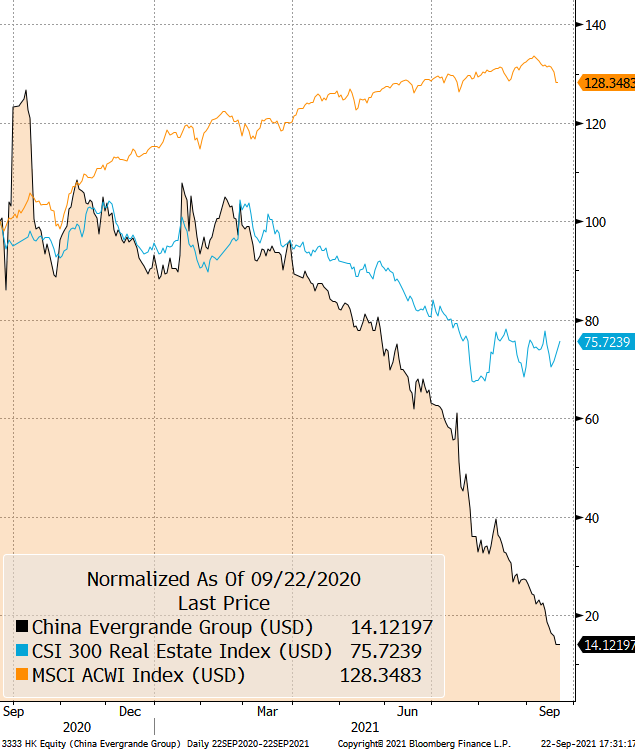

Financial markets have been in a bit of turmoil this week for Evergrande, a Chinese real estate company, which exploded on the crest of the Dragon boom.

She is very big, heavily in debt (around $ 300 billion, according to the news) and owns a football team, which certainly suggests something about her investment approach and why she is in an awkward financial position today.

The company is having some cash flow problems and may be insolvent, at least on some of its debt. This is a typical case of corporate mismanagement that resulted in a liquidity crisis. In the last market year, the company had made significant profits. Now, thanks to excessive use of loans, some wrong investments and the effects of the pandemic, the giant could be in difficulty in repaying part of its debts and this would lead the company to bankruptcy due to lack of liquidity.

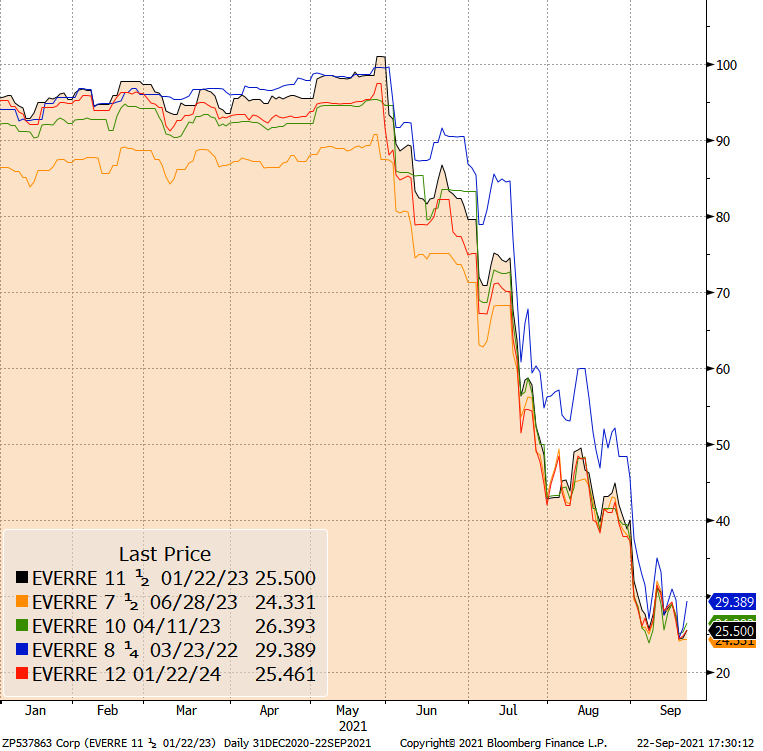

The story is then seasoned by the uncontrolled issuance of debt securities to individuals and financial companies, some of which are also trimmed to suppliers and ordinary citizens who now risk having to line up to hope to see their credits repaid. The company's bonds are already considered as waste paper and are traded for amounts close to 20 cents per dollar, the values of a company practically in default.

In short, many of the structural vices of Chinese capitalism seem to meet in this story:

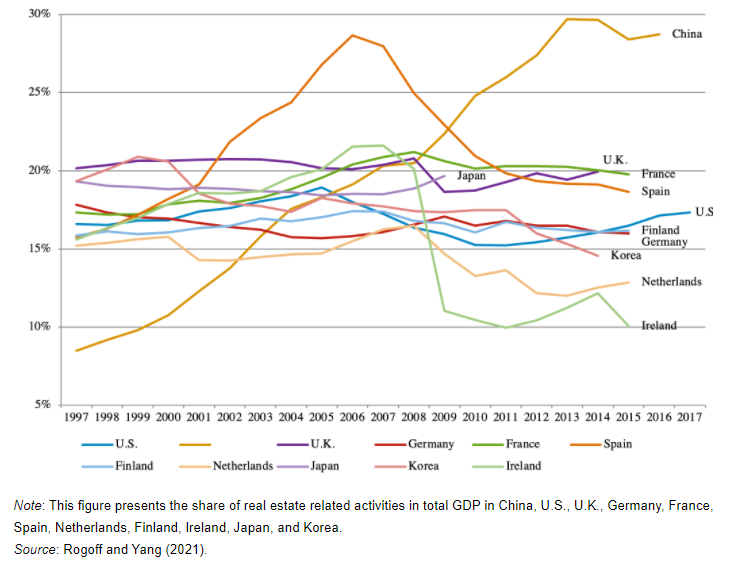

First of all, a real estate sector that has grown hypertrophically and has become too large even in relation to the abnormal size of the Chinese economy.

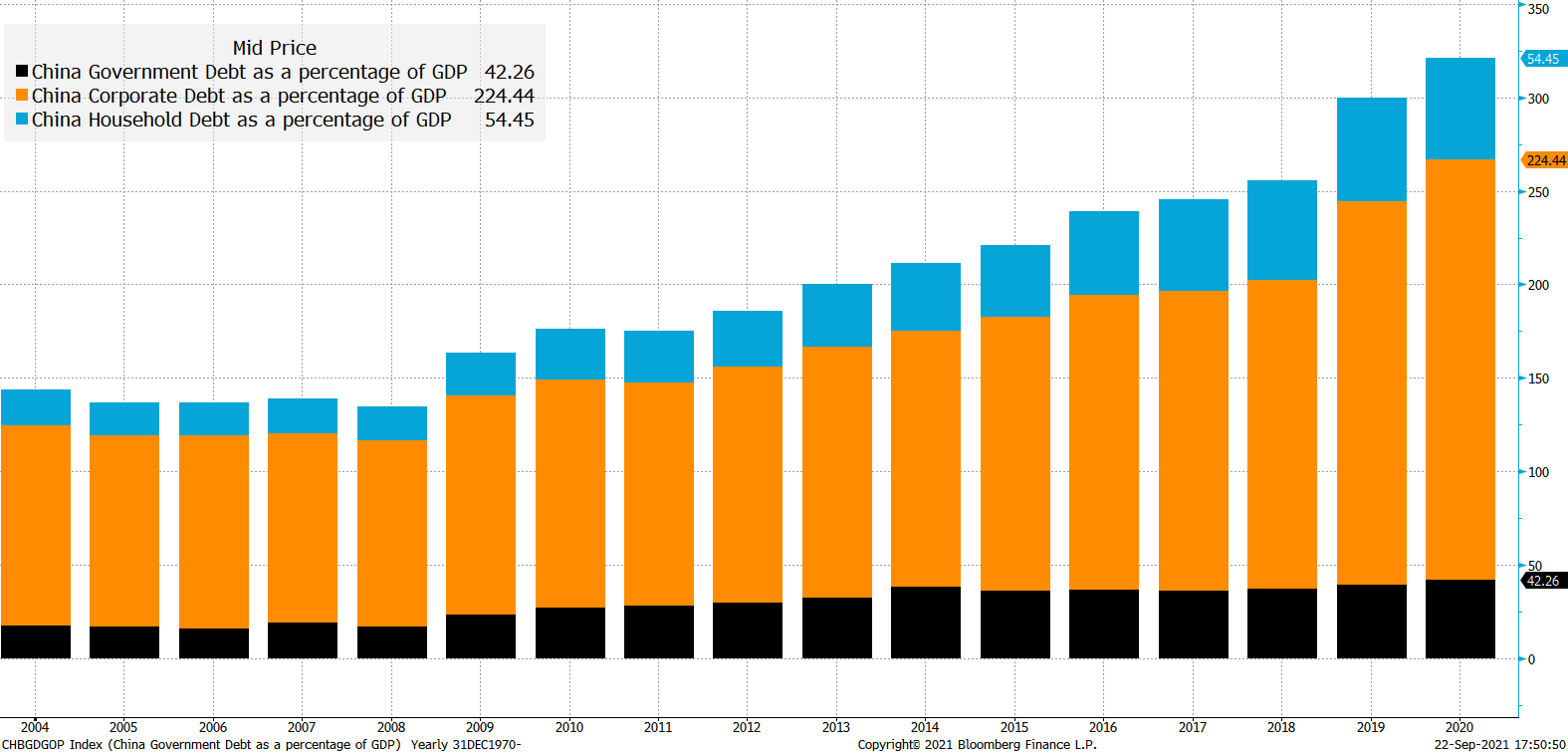

And then a high recourse to private debt to finance economic growth, however, in a regulatory environment that is not fully mature.

All in a context in which Xi's government is intervening to redefine the scale of power between public and private and try to remedy the excesses of economic growth, also placing regulatory limits on the possibility of growing in debt. In recent months, we have seen the state take action against, among other things, private education, video games and the culture of celebrity. In the case of the real estate sector, the state has acted to try to curb excessive leverage through a series of rules. It could be argued that Evergrande is a test case for the effectiveness of such rules.

All of these decisions have had a negative impact on share prices in various sectors of the Chinese economy (private companies operating in the education sector, Macau casinos), but especially large tech companies. Also on the bond side we had begun to notice turbulence and at the end of August we had highlighted the Huarong affair.

To this substrate of regulatory uncertainty was added the theme of the slowdown of an economy that needs to continue running at full speed to avoid engulfing the risks, large and small, inevitably linked to its maturation process.

Beyond the general macroeconomic considerations, what really worries the markets in the short term are, firstly, the potential systemic value of an eventual Evergrande bankruptcy and, secondly, the signals that this industrial crisis sends us about the health of the Chinese economy.

As regards the first point, many commentators have gone so far as to imagine a comparison with the Lehman Brothers affair: it seems to us a risky comparison for various reasons. First of all, the size of the exposure (300 billion against the more than 500 billion of the American investment bank). Second, the greater interdependence of the American financial system with respect to the Chinese industrial system, recalling the perverse effect of the structured instruments that served to send the financial system into a tailspin. The political climate, with a government – the Chinese one – which today has many more options and a greater capacity to act than the US government in 2008. Even if, just yesterday, the Chinese central government appeared unwilling to bail out in a big way and has asked local officials in the country to prepare for a "possible storm". For his part, in a note, the president and founder Hui Ka Yan assured that "the company will do its best to resume work and production".

That said, Evergrande has a systemic role that is certainly superior to that of, for example, the technology companies that have ended up in the eye of the storm in recent months, despite a lower capitalization.

Evergrande has 20 billion dollar bonds outstanding and is the largest issuer of high yield dollar bonds in Asia. As for the onshore market, the company has around 7 billion euros of bonds in circulation. Evergrande is then exposed for over $ 50 billion to the Chinese banking system. This is a relatively small share compared to the total debt position in which trade payables to suppliers dominate. In this sense, the greatest risks could spill more on the real economy than on the financial system.

Evidently, any event that could slow down the Chinese economy is a cause for concern for all investors. The uncertainty Evergrande is already part of a picture that sees the activity of the real estate sector slow down in the second half of the year, together with the rest of the economy, which after having overcome 2020 better than other countries, is in a state of fatigue.

How will this affair end?

When a company goes bankrupt, causing risks to the community, the state has three main paths ahead: nationalization, bail out and market solution (hence bankruptcy).

We believe that the Chinese government has, in any case, the capacity to intervene should this prove necessary. Furthermore, its field of action is not limited either by the need to respond to the demands of the electorate or by the prejudice, still present in the West, about a possible nationalization. The aforementioned case of Huarong, in which public intervention was followed by the takeover of the company by a consortium of state-owned companies, is a relevant precedent.

All of this gives hope for a "managed solution" of some kind. If it does occur, market volatility should dissipate, although Chinese growth may slow. In itself, no analysis can help to make predictions, investors generally make choices according to a binary pattern: on the one hand, those who believe that eventually the Chinese government will be able to manage this and other similar situations in the future effectively, on the other. those who believe that the situation will get out of hand.

For what it's worth, we'd say that history has so far been on the side of the government and its ability to handle these kinds of problems. However, we cannot underestimate the complexity of the Chinese system.

For our part, we therefore continue to believe, despite a positive outlook for the Chinese economy, that a decisive bet on Dragon equities is still premature. On the other hand, we continue to be satisfied with the performance of government bonds that we included in our portfolios in January and which moved against the trend of the increase in market risk (acting as a safe haven) further proof of maturity. of this asset class.

In general, even in light of the market positioning with relatively high valuations, the case of Evergrande is another brick that enriches the risk wall. It will certainly be an element to consider in the positioning of portfolios from here on out.

This is a machine translation from Italian language of a post published on Start Magazine at the URL https://www.startmag.it/economia/perche-il-paragone-fra-evergrande-e-lehman-e-azzardato-report-moneyfarm/ on Mon, 27 Sep 2021 06:28:23 +0000.